The customer-centric revolution has finally reached the insurance industry. Slowly and sometimes reluctantly, large insurance carriers realized that confusing forms written in archaic language frustrated their customers, who perceived the industry giants as only trying to protect their own interests. After all, most carriers didn’t even refer to them as customers; they were “policyholders” or “claimants.”

But that has changed significantly, especially in the past 15 years. While industry pioneers like GEICO and Progressive took a more customer-focused and “friendly” approach to catapult their personal lines business, many of the largest carriers now boast a Chief Marketing Officer, Chief Customer Officer, or Chief Engagement Officer. Those senior titles were practically unheard of 20 years ago.

This shift—from an institutional, legacy view to an external, customer-focused perspective—is timely, because the demographics of insurance buyers are changing.

The case for digital transformation in insurance

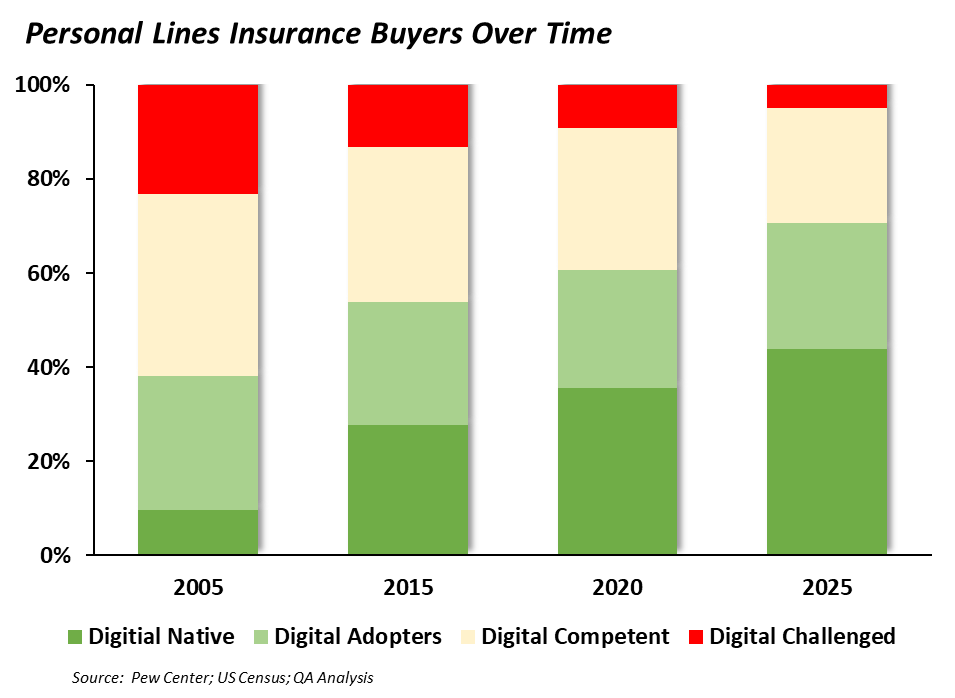

Consider the following chart, which reflects the purchasers of personal lines (auto, homeowners, renters, etc.) insurance from 2005 actual to 2025 forecast.

Buyers are becoming more digitally adept. This trend is not simply driven by age, as Gen X/Yers and Millennials overtake their less tech-savvy parents and grandparents. Older generations are becoming more digitally proficient, too, and many a grandparent today is as adroit with Facebook and online shopping as their grandkids are. So, while the population shifts to a younger generation of insurance buyers, the growing technological sophistication of earlier generations is accelerating the trend.

Today’s insurance consumers can be broken into four groups:

- Digital Native: these buyers grew up with or have become comfortable with digital “ubiquity.” The internet has always been a part of their life and interacting with sellers online is fundamental, if not “old school.” In fact, they expect to be able to interact with companies anywhere, on any digital device (smartphone, tablet, Alexa/Echo devices, etc.), with lightning speed and zero complexity. These buyers aren’t impressed with a quote in “15 minutes or less”—they want it in 60 seconds or less. While powered by the influx of Millennials (born ~1980-1996) and Gen-Z (born after 1996) into the insurance marketplace, they are augmented by many Gen-X (born 1965-1979) who came of age in the PC era and some Baby Boomer (1946-1964) technophiles.

- Digital Adopters: with Gen-X and early Gen-Y as their largest core, digital adopters have come to expect most, if not all, of the ease and simplicity of ubiquitous digital interaction as the Natives. They may, however, be less reluctant than the Digital Natives to resort to an actual phone call to a carrier.

- Digital Competent: while this group may not have come of age with PCs and smartphones, they have grown accustomed to and comfortable with emerging technologies. They may not handle every brokerage or banking transaction online or by smartphone app, but they know how to. Even though they may still read a physical paper (sometimes just out of nostalgia), they are regularly reading their morning news on the train on a Kindle or iPhone.

- Digital Challenged: this group prefers the old ways of interacting with their carrier or agent—by phone or even in person—and eschews (or distrusts) most things digital. They may pay by check (or cash) rather than ACH or credit card, and they want to speak with a person, not some “interactive voice response” system. The dwindling number of the digitally challenged is partly driven by the passing of the Silent Generation (born prior to 1945) but also by steadfast technophobes and those wary of digital transactions in general.

The importance of this customer evolution for insurers is clear. Currently, over 50% of personal lines buyers (Digital Natives and Digital Adopters) have high expectations for a concrete, pervasive, simple, purposeful, and engaging digital customer experience. That’s up from under 40% just 10 years ago. By 2025, they will represent more than 70% of insurance buyers. Carriers who do not embrace those changing demographics—and take on the cause of digital transformation—are apt to be left in the “digital dust.”

The urgency of digital transformation in insurance

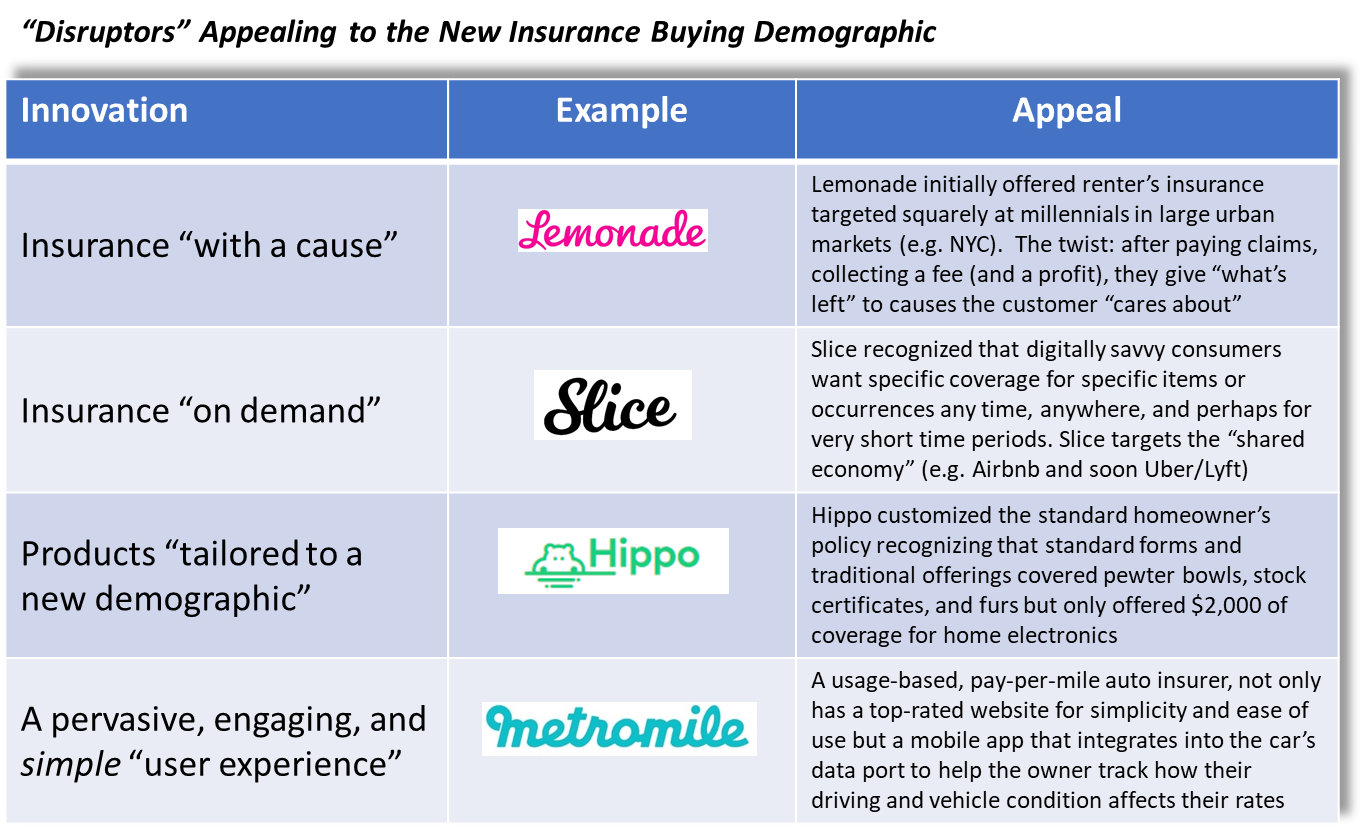

Given the shift in demographics, digital expectations, and a desire to change what’s perceived as “wrong” with traditional insurance, it is no surprise that a new group of “disruptors” is emerging. Some of these startups are well-funded or mainstream carrier backed, and many of them claim to “reimagine” the insurance experience and eliminate unnecessary complexity in the process. These startups can seem daunting to traditional carriers. They leverage InsurTech innovations such as artificial intelligence and big data to improve and perhaps mechanize underwriting and product development. They offer a digital-only or digital-heavy customer experience to bypass physical agents or help manage claims. And they design digital-centric user interfaces and customer-focused user experiences. Here are a few examples:

Rather than viewing these startups as foreboding harbingers of rampant disintermediation, job loss, or doom, traditional carriers can and are learning from some of the best-in-class innovators who are “plugging into” the new insurance buyer’s psyche. Many insurers are already using InsurTech advances developed in-house or through technology partners. However, to date, most big-carrier InsurTech applications have been aimed at cost/headcount reduction and efficiency gains. Robotic process automation helps eliminate rote tasks and clerical labor, “Big Data” and AI enhance the accuracy of pricing and underwriting, drones help assess damage and improve claims adjustment.

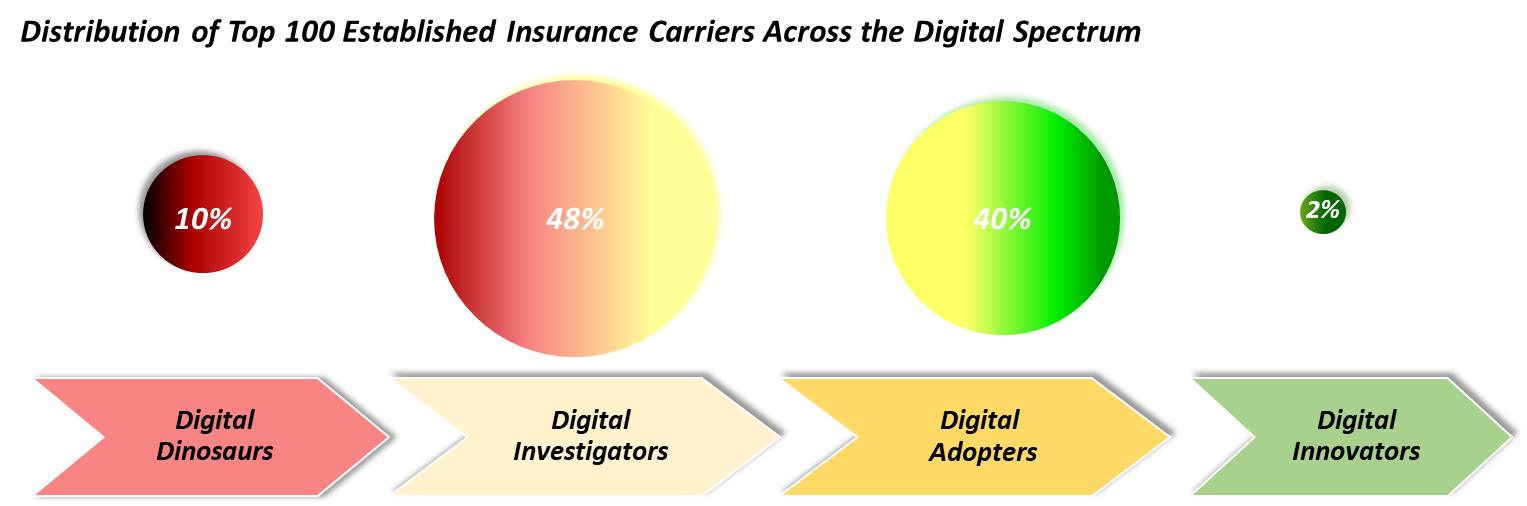

But very few of the largest insurers have undergone the comprehensive digital transformation that’s needed to truly meet the needs and desires of this emerging customer demographic. A recent survey I conducted of P&C insurance executives bears this out:

Only a handful of insurers—the Digital Innovators—have implemented a cohesive and truly innovative digital customer experience. Meanwhile, 88% of insurers are either investigating or partially implementing digital customer experience strategies. However, many programs labeled “digital strategy” are still internally focused: trying to leverage data and communication to improve internal or legacy KPIs, metrics, and processes. They are not externally focused on the customer experience and evolving customer needs.

Digital Adopters, 40% of the sample, have taken some steps towards innovative digital engagement. They may have built enhanced online user interfaces or smartphone apps, for instance. But often they are merely “shining a sneaker” rather than acting like digital disruptors. Digital Investigators, meanwhile, are actively developing use cases, business cases (ROI), and prototypes, but they seem to be moving glacially, allowing ideas to get stymied in bureaucratic committees.

Finally, about 10% of large, traditional insurers (Digital Dinosaurs) either don’t have the requisite capital or the inclination to innovate; they are simply burying their heads in the sand. Some are content to focus on a declining customer segment that has no use for a digital solution (or at least a digital experience when it comes to insurance). This last group is pursuing what’s called a “last iceman strategy”—though there may not be much demand for ice delivery anymore, the sole surviving iceman does have a monopoly of that small market. For such a strategy to succeed in insurance, the last large player will have to have market dominance, given that the segment is likely to account for just 5% of insurance purchases by 2025, and is shrinking fast.

What digital transformation in insurance looks like

Pursuing a bona fide digital strategy has two core aspects. First, it is outward-looking, focused on emerging customer needs and preferences rather than internal needs like legacy processes, products, and reporting. Second, it is pervasive. It incorporates all elements of the value chain, from payments processing to regulatory reporting and compliance to historically mundane back-office operations—not just product development, pricing, underwriting, and claims. A digital strategy is not developing a new, “hip,” snazzy website or launching a smartphone app. Improving and tailoring the customer engagement experience is vital, but improved user interface (UI) and user experience (UX) alone will fail if underlying processes, approaches, and thinking do not embrace a pervasive digital approach.

Established carriers can learn from, adopt, and improve upon startup InsurTech innovations, much as they did in the e-commerce era. But the demographics alone dictate that insurers move out of committee and into action. Ultimately, it may be less about “reimagining insurance” than refining, evolving, and adjusting to a digital world. Because when it comes to customer expectations and needs, the digital era isn’t coming—it’s here.

This post first appeared at Quincy Analytics.

Get the Skills You Need

Thousands of independent consultants, subject matter experts, project managers, and interim executives are ready to help address your biggest business opportunities.

About the Author

More Content by Brian Kelley